About Roth Conversions

Understanding Roth Conversions

To understand a Roth conversion, you first need to understand what a traditional IRA is and how it functions over time.

A traditional IRA holds money that has not yet been taxed (pre-tax). This money grows tax-deferred, which means you don’t pay taxes on the growth until you withdraw the funds. You’ve probably heard this before, but what does it really mean?

A helpful way to think about a traditional IRA is as a joint account between you and the government. The government’s share of this account corresponds to your tax rate at the time of withdrawal; their "ownership" depends on your tax bracket

Let’s assume your IRA grows over your lifetime, which is good because it means more assets for you. However, the government ultimately wants its share. To enforce this, the IRS requires you to take minimum withdrawals called Required Minimum Distributions (RMDs); Starting at age 73. The RMD amounts are based on a life expectancy table, but as a rough estimate, you might withdraw about 4% of the account balance at age 73, increasing to around 8% by age 90. For more detail, see IRS Publication 590-B.

As your IRA balance grows, these RMDs, which are taxed as ordinary income, can become a burden, especially if you must withdraw more than you actually spend. Keep in mind you may also have income from Social Security, pensions, or other sources. Large withdrawals can push you into higher tax brackets and may increase your Medicare IRMAA surcharge and increase the government’s share of your IRA.

One way (not the only) to mitigate this issue is through a Roth conversion. This involves converting pre-tax money from your traditional IRA to a Roth IRA. Roth accounts are funded with after-tax money; you pay taxes upfront. The big advantage is that Roth money grows tax-free and you are never required to take RMDs from the Roth account; the government has no stake in your Roth.

When you convert pre-tax funds to a Roth IRA, you pay taxes at your current rate on the amount converted. If you have reached RMD age, you must first satisfy your RMDs before converting any additional funds to Roth.

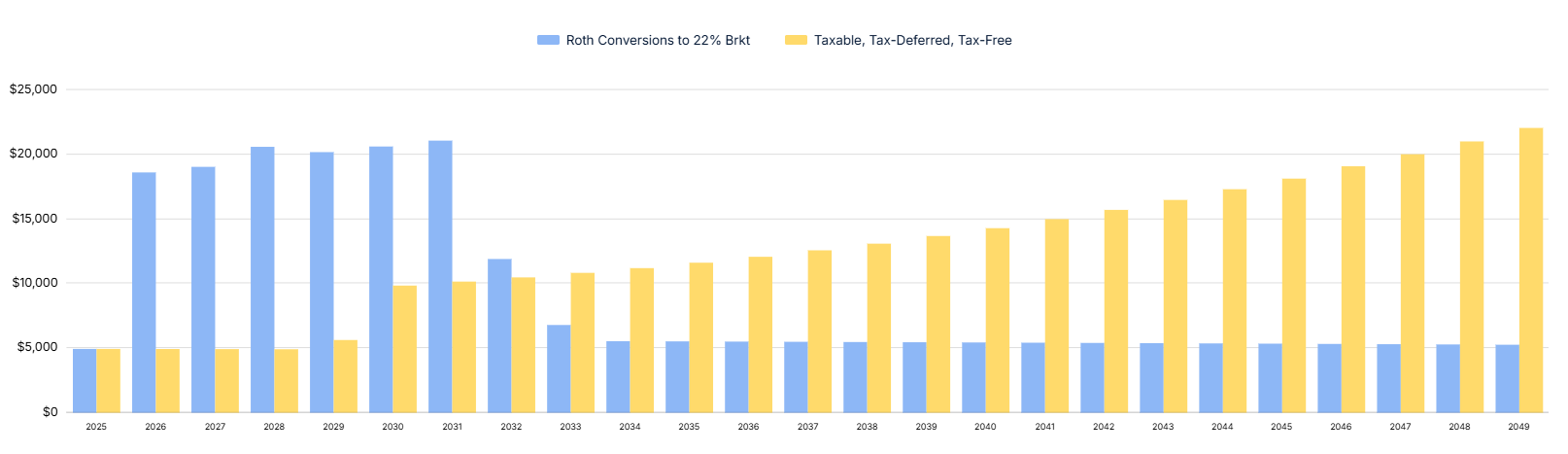

Figure 1 example of taxes paid each year of a retirement plan (yellow) vs Roth conversion (blue)

Your situation is unique from others and requires careful analysis. We use multiple software tools and consult with your CPA before recommending a Roth conversion (all part of comprehensive planning). While conversions increase your tax bill in the year of conversion, they can reduce your lifetime tax burden. However, Roth conversions are not always the best choice and should be evaluated carefully.

There are some strategic opportunities for Roth conversions:

Periods of little or no income: Such as between jobs, when your tax rate is lower, can be an ideal time for conversions.

Market downturns: Converting investments to Roth when their value has declined (and is expected to rebound) can reduce the tax impact of the conversion.

Retiring before 73: Even though you’ll most likely be withdrawing from your IRA, your tax rate is probably lower than when working and later in life when RMDs may be higher than your income needs.

There are some other considerations to know if a Roth Conversion is right for you. With the OBBBA (One Big Beautiful Bill act), and the many below the line deductions, Roth conversions can raise AGI (adjusted gross income) which might phase you out SALT (state and local tax) cap limits and the over 65 extra standard deduction. Careful tax analysis is a must. Another consideration is how you would want your beneficiaries to inherit money. With any (Roth or traditional) inherited IRA, the balance must be taken out within 10 years. For traditional inherited this is usually done in chunks every year for 10 years as there are tax considerations for taking it out in one year. For an inherited Roth IRA, that money can grow for anther 10 years and be taken out as a lump sum with no taxes. Or it could be drained year 1 as there are no tax consequences. How you want your beneficiary to inherit the money may hold a different weight for you. Likewise, you may have opinions on “paying the tax” for the money you leave behind.

There are many facets to the Roth conversion and know what’s best for you requires deep understanding of your unique situation. The decision is more than just numbers and we are here to guide and support you through the complex maze.